On October 17, 2024 A&W Revenue Royalties Income Fund (symbol: AW-UN.TO) and A&W Food Services of Canada Inc. (symbol: AW.TO) completed a reorganization, resulting in A&W Revenue Royalties Income Fund units being exchanged for a combination of cash and shares of A&W Food Services of Canada Inc..

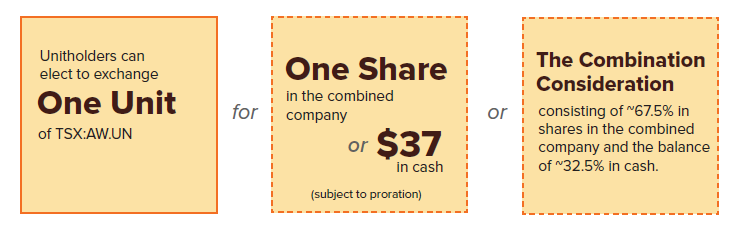

Prior to reorganization, AW-UN.TO unitholders could elect to receive different combinations of cash and AW.TO shares, subject to proration. If you were a AW-UN.TO unitholder subject to the reorganization, please refer to your brokerage transaction records to determine the actual number of AW.TO shares and/or cash that you received.

A&W Revenue Royalties Income Fund published a Management Information Circular document on September 3, 2024 containing details on the tax treatment of the reorganization for Canadian investors.

The tax treatment of the reorganization depends on whether you have made a Section 85 Election. This election provided the potential opportunity to receive the newly issued A&W Food Services Inc. shares on a tax-deferred basis. The Section 85 Election was due to be filed on October 4, 2024.

Let’s illustrate the tax treatment for both scenarios (with and without a Section 85 Election) using the following example

- You purchase 1,000 shares of AW-UN.TO settling on June 4, 2024 for a price of $29.00/unit (no commission).

- On October 17, 2024 your 1,000 units of AW-UN.TO are exchanged for 973 shares of AW.TO, plus a total of $995.00 in cash.

- We’ll assume a fair market value (FMV) for AW.TO of $38.00 per share at the time of the exchange, based on the opening market price of AW.TO on October 18, 2024.

- The $995.00 in cash received as part of the exchange does NOT include the final cash distribution for AW-UN.TO of $0.1052 per unit (taxable as a non-eligible dividend).

Please note that the dollar and unit/share ratios found in this example may not correspond to the values in your particular case. Refer to your brokerage documents for the actual cash and number of AW.TO shares received.

No Section 85 Election

For the case where you did not make a Section 85 Election, the Management Information Circular Document states the following (page 131):

A Resident Holder that (a) disposes of Units pursuant to the Transaction and (b) does not make a Section 85 Election, will be considered to have disposed of the Units for proceeds of disposition equal to the sum of (i) the aggregate amount of cash received on the disposition, and (ii) the fair market value of the A&W Food Services NewCo Shares received on the disposition. As a result, the Resident Holder will realize a capital gain (or a capital loss) equal to the amount by which such proceeds of disposition, net of any reasonable costs of disposition, exceed (or are less than) the adjusted cost base to such Resident Holder

of the Units immediately before their disposition.

Also:

The aggregate cost to a Resident Holder of A&W Food Services NewCo Shares acquired pursuant to the Transaction will be equal to the fair market value of the A&W Food Services NewCo Shares as at the time of acquisition.

For the example above with no Section 85 Election, you are deemed to have sold your AW-UN.TO units for a total amount equal to the FMV of the AW.TO shares received plus the cash received:

Proceeds of Disposition = ($38.00/share x 973 shares) + $995.00

= $37,969.00

The cash amount of $995.00 does not include the final cash distribution of $0.1052 from the AW-UN.TO units.

You are deemed to have acquired the 973 shares of AW.TO at a cost equal to the FMW, or $38.00/share.

This can be inputted into AdjustedCostBase.ca with the following transactions:

- A “Buy” transaction on June 4, 2024 for 1,000 shares of AW-UN.TO for an amount of $29.00/share.

- A “Sell” transaction on October 17, 2024 for 1,000 shares of AW-UN.TO for a total amount of $37,969.00. This results in a capital gain of $8,969.00 ($37,969.00 less $29,000.00).

- A “Buy” transaction on October 17, 2024 for 973 shares of AW.TO for an amount of $38.00/share.

With a Section 85 Election

For the case where you have made a Section 85 Election, the Management Information Circular Document states the following (page 131):

A Resident Holder that (a) is an Eligible Holder, (b) disposes of Units pursuant to the Transaction for consideration that includes A&W Food Services NewCo Shares, and (c) validly makes a Section 85 Election as contemplated herein in respect of the disposition of the Units (an “Electing Resident Holder”), may defer all or a portion of any capital gain otherwise arising on the disposition of Units depending on the Elected Amount (as defined below) and the adjusted cost base to the Eligible Holder of the Units immediately before the disposition, as described a further detail below.

…

Subject to the limitations generally described below, the Elected Amount will be treated for the purposes of the Tax Act as the Electing Resident Holder’s proceeds of disposition of their Units. In general, the Elected Amount for an Electing Resident Holder is subject to the following limitations:

(a) the Elected Amount may not be less than the aggregate amount of cash consideration received for the Units;

(b) the Elected Amount may not be less than the lesser of (i) the adjusted cost base to the Electing Resident Holder of the Units disposed of and (ii) the fair market value of such Units, in each case determined at the time of disposition; and

(c) the Elected Amount may not be greater than the fair market value at the time of the disposition of the Units disposed of.

…

The tax treatment for the disposition of Units by an Electing Resident Holder generally will be as follows:

(a) the Electing Resident Holder will be deemed to realize proceeds of disposition for the Units equal to the Elected Amount;

(b) if the proceeds of disposition are equal to the aggregate of the adjusted cost base to the Eligible Holder of the Units, determined immediately before the disposition, and any reasonable costs of disposition, no capital gain or capital loss will be realized by the Eligible Holder;

(c) the Electing Resident Holder will realize a capital gain (or a capital loss) equal to the amount by which such proceeds of disposition, net of any reasonable costs of disposition, exceed (or are less than) the adjusted cost base to such Electing Resident Holder of the Units immediately before their transfer to A&W Food Services NewCo; and

(d) the aggregate cost to the Electing Resident Holder of A&W Food Services NewCo Shares received as consideration for the Units will be equal to the amount by which the proceeds of disposition of the Units exceeds the aggregate amount of cash received as consideration for the Units.

Returning to the previous example, we’ll assume an Elected Amount equal to the ACB of the AW-UN.TO shares immediately prior to the reorganization, or $29,000.00. This Elected Amount will result in a full deferral of the capital gain, and adheres to the restrictions above.

In this case, the proceeds of disposition for the AW-UN.TO are equal to the Elected Amount, or $29,000.00. This results in a capital gain of $0. The AW.TO shares received are deemed to be acquired for the Elected Amount less the cash received as part of the disposition:

Cost of AW.TO shares = $29,000.00 - $995.00

= $28,005.00

The cash received from the final distribution of $0.1052 per unit from AW-UN.TO is not subtracted from this cost amount.

The above example, assuming that a Section 85 Election has been made with an Elected Amount of $29,000.00, can be inputted into AdjustedCostBase.ca with the following transactions:

- A “Buy” transaction on June 4, 2024 for 1,000 shares of AW-UN.TO for an amount of $29.00/share.

- A “Sell” transaction on October 17, 2024 for 1,000 shares of AW-UN.TO for a total amount of $29,000.00. This results in a capital gain of $0.

- A “Buy” transaction on October 17, 2024 for 973 shares of AW.TO for a total amount of $28,005.00

So, it looks like if you did not elect the Section 85, you have a gain (or loss) to declare for all the Income Fund shares you owned and “sold”, based on your Broker’s Statement. The cost of a new Food Services Inc. share is your Broker’s Statement amount divided by the new number of shares you received. (which is 973 in your example)

Correct?

Sally,

Yes, if you didn’t make the election then you are deemed to have disposed of the AW-UN.TO units for an amount equal to the FMV of the AW.TO shares plus the cash received (excluding the final distribution), and deemed to have acquired the AW.TO shares for their FMV.

If the cost shown on your brokerage statements for the AW.TO seems reasonable (approximately equal to the market price of the AW.TO shares at the time of the reorganization) then it makes sense to align with this value. But I would suggest sanity checking the value to ensure that it’s reasonably close to what you’d expect. For example, a brokerage may not be aware of who has made the election and might by default base of the cost of the AW.TO shares on the ACB of your AW-UN.TO units (which itself may not be accurate). Or they might use the market price for AW.TO shares from some arbitrary date following the reorganization, or may fail to properly accounting for the cash component, for example. If the cost that your brokerage has assigned to your AW.TO shares does not seem reasonable, then I would suggest calculating it yourself.

Thank you for your help. I have one more query about the tax implications of the High Arctic Energy Services reorganization in August and the ACB of the New High Arctic Energy Services NewclA and the High Arctic Overseas Holdings Corp.

Sally,

For High Arctic Energy Services’ reorganization effective on August 12, 2024, $0.76 per share of return of capital was distributed, and each share was then exchanged for 0.25 shares of High Arctic Overseas Holdings Corp. (SpinCo) plus 0.25 shares of New High Arctic Common Shares.

High Arctic Energy Services published a Management Information Circular document on May 13, 2024 that highlights the taxable of the reorganization:

https://www.sedarplus.ca/csa-party/records/document.html?id=387aad6c8a91ec088510592472ad5bf488866eec8edca48bea7faba147292ca0

See the following on page 56:

Also, High Arctic Energy Services has suggested a FMV of $1.755 per share of High Arctic Overseas Holdings Corp. (SpinCo) at the time of the reorganization:

https://haes.ca/2024-reorganization/

Assuming that the total FMV of the High Arctic Overseas Holdings Corp. shares received does not exceed your total ACB of your High Arctic Energy Services shares immediately prior to the reorganization, then the following transactions can be inputted into AdjustedCostBase.ca for the reorganization:

Alternatively, if you would like to represent both the old High Arctic Energy Services shares and the New High Arctic Common Share with the same security, the following set of transactions can be used:

The amounts and split ratio for the above transactions may need to be altered in the case where you received cash in lieu of fractional shares.